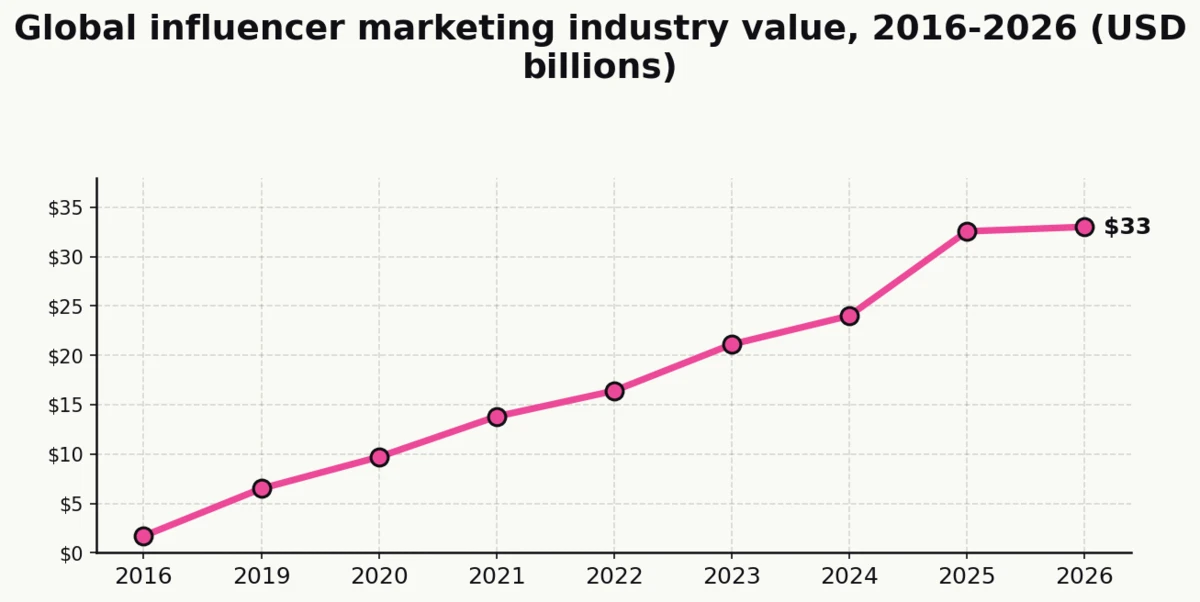

The global influencer marketing industry is on pace to hit $33 billion in 2026, nearly twenty times its size a decade ago, and the checks brands are writing keep getting larger.

Nearly nine in ten US marketers now run influencer campaigns, the average brand works with a roster of creators rather than a single marquee hire, and the category has moved from a test-budget line item into a permanent column on most media plans. At the same time, close to six in ten brands say they ran into some form of fraud last year, and measurement of what those dollars actually return still varies wildly by platform and creator tier.

Below is the freshest read on where the category stands in 2026: the market’s size and growth, the shift in platforms, the widening gap between nano and mega creators, how consumers actually behave, and how creators are now showing up at live brand activations (the piece most of the incumbent stats pages miss).

Top Influencer Marketing Statistics (Editor’s Picks)

- $33 billion — projected size of the global influencer marketing industry in 2026, up from $24 billion in 2024 and $1.7 billion in 2016.

- 86% of US marketers ran an influencer campaign in 2025.

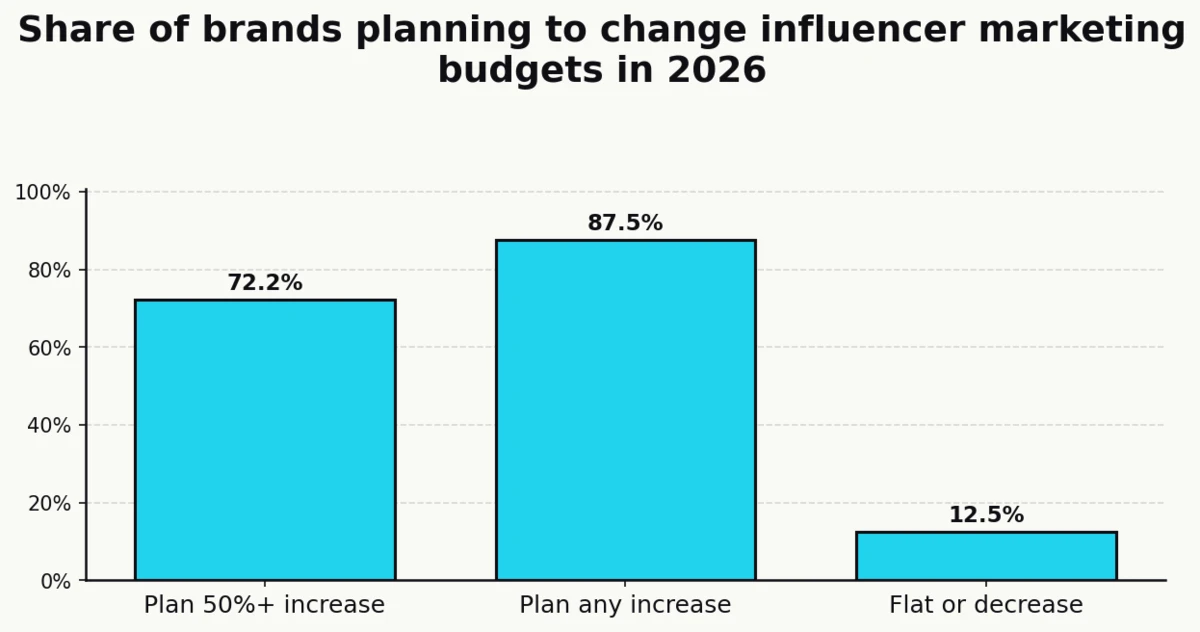

- 72.22% of brands plan to raise their influencer marketing budget by 50% or more in 2026.

- 31% of brands now name TikTok as their preferred influencer platform, with Instagram and YouTube close behind.

- 2.53% average engagement rate for Instagram nano-influencers, nearly three times the 0.92% rate seen on mega-influencers with more than a million followers.

- 59.8% of brands reported experiencing some form of influencer fraud in 2024, up from 55% a year earlier.

- 69% of consumers say they trust a recommendation from a friend, family member, or influencer over a direct brand message.

- 61% of consumers now find relatable creators most appealing; only 11% still prefer celebrity influencers.

- 87.68% of TikTok influencers are nano-tier, with fewer than 10,000 followers.

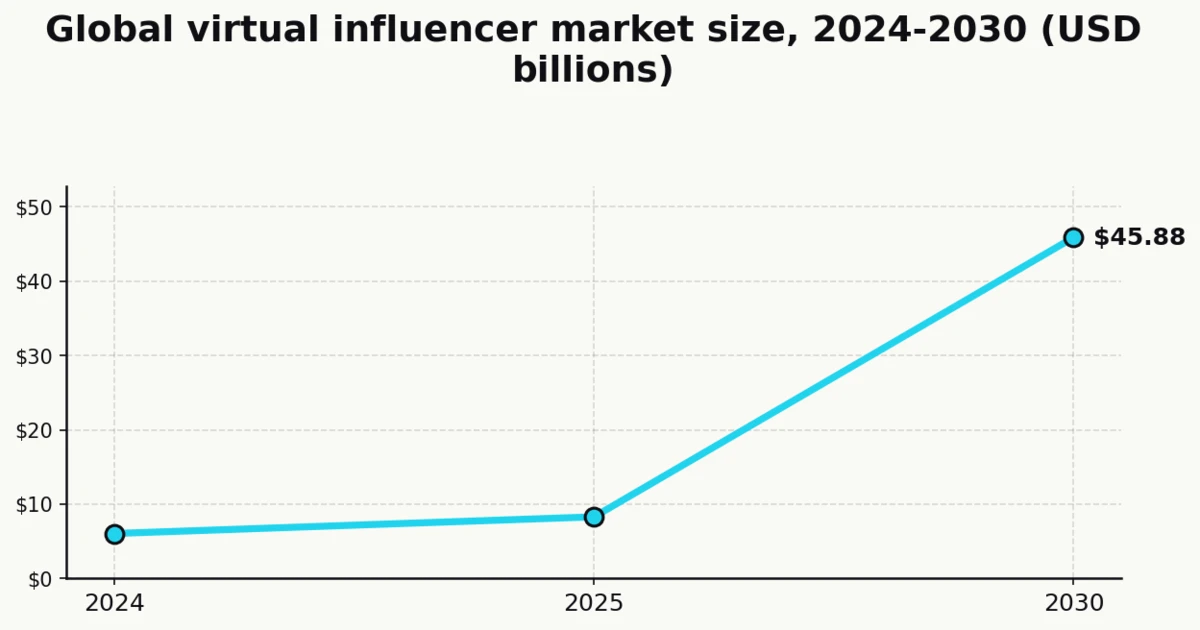

- $45.88 billion — projected value of the global virtual influencer market by 2030, at a 40.8% compound annual growth rate.

Market Size and Growth

After a $24 billion calendar-year 2024, the influencer marketing category heads into 2026 with double-digit growth still intact. The budget line is no longer an experimental allocation. It sits alongside paid search, paid social, and display on most consumer-brand media plans, and is beginning to appear on B2B ones as well.

The category also sits inside a much larger creator economy that investment banks now forecast into the hundreds of billions of dollars. Influencer marketing is the slice where brands put real paid-media dollars, and every credible forecast points up.

The global influencer marketing industry is projected to hit $33 billion in 2026 (Influencer Marketing Hub)

The Influencer Marketing Hub’s 2026 Benchmark Report, built from a survey of roughly 3,000 brand-side marketers and agency partners, projects the industry at $33 billion in 2026, a nineteen-fold increase since 2016, when the category was valued at just $1.7 billion.

The growth curve has been remarkably steady. IMH’s multi-year series places the industry at $9.7 billion in 2020, $21.1 billion in 2023, $24 billion in 2024, and $32.55 billion in 2025 before this year’s update. That consistency is what keeps the category linkable: every year the headline number ticks up, and every year journalists, analysts, and trade press quote it.

Budgets reflect the trajectory. 85.8% of brands now plan a dedicated influencer marketing budget, up from roughly 37% in 2017, and 72.22% of surveyed brands plan to raise that budget by 50% or more in 2026.

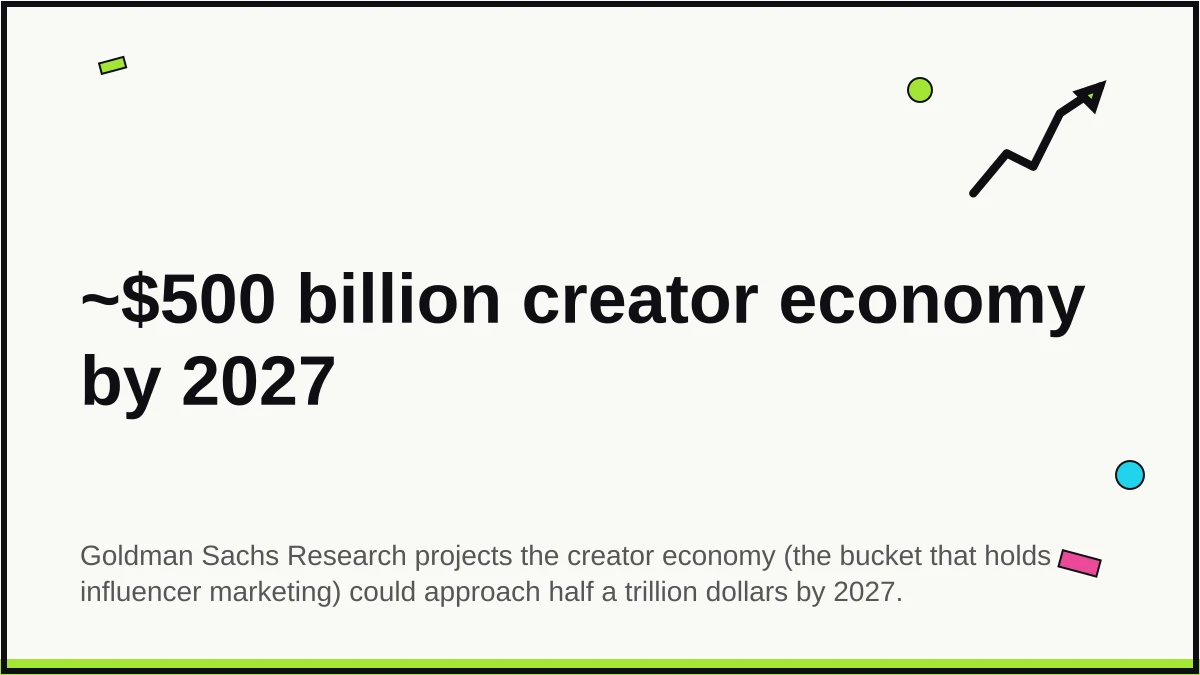

The creator economy could approach half a trillion dollars by 2027 (Goldman Sachs)

Goldman Sachs Research projects the total creator economy, a bigger bucket that includes brand deals, direct platform payouts, merchandise, and subscription revenue, could approach $500 billion by 2027, up from a baseline of roughly $250 billion.

Influencer marketing is the subset of that total where brands spend paid-media dollars on creator partnerships. It currently makes up roughly 10% of the full creator economy, and it is the slice most visible to CMOs who need to defend a line item on the P&L.

The virtual influencer market is projected to reach $45.88 billion by 2030 (Grand View Research)

Grand View Research sizes the 2024 virtual influencer market at $6.06 billion, growing to $45.88 billion by 2030 at a 40.8% compound annual growth rate from 2025 onward.

North America accounts for more than 42% of 2024 revenue, and human-avatar formats (digital personas that resemble real people) account for 68% of the market. The category is still small next to human influencer marketing, but no other subsegment is growing at anywhere near 40% per year.

26% of marketers now allocate more than 40% of their total marketing budget to influencer partnerships (Sprout Social)

Sprout Social’s 2025 research places more than a quarter of marketers among the high-concentration group, pushing the bulk of their paid-media budget into creators. That share would have been unthinkable in 2020, when the average brand still treated influencer marketing as an experimental slice of social.

The concentration is most pronounced in consumer goods, fashion, beauty, and gaming, where creator partnerships now outperform traditional paid social on attributed conversion rate and cost per acquisition. In those verticals, the question has flipped from “should we add creators” to “what is left for non-creator channels.”

Sources: Influencer Marketing Hub, Goldman Sachs, Grand View Research, Sprout Social.

Adoption and Brand Usage

Influencer marketing has graduated from experimental test budget to table-stakes channel. Adoption hit a supermajority this year, and the share of brands running campaigns with a roster of creators rather than a single marquee hire continues to rise.

86% of US marketers ran an influencer campaign in 2025 (Sprout Social)

Sprout Social’s 2025 analysis places US marketer adoption at 86%, high enough that “does your brand do influencer marketing?” is no longer a useful screening question on a media-agency RFP. The working assumption is yes.

Breakdowns by business model show 57.6% of brands running influencer programs also operate a direct-to-consumer ecommerce store, per Influencer Marketing Hub reporting. That tight correlation between influencer spend and attributable sales is one of the main reasons the category kept growing through the 2022-2024 DTC correction.

Inside the marketing organization, 66.33% of brands now run their influencer programs in-house rather than through an agency, per the same Influencer Marketing Hub survey series. A nearly two-thirds in-house majority is itself a sign of category maturation: brands build the capability internally once the line item is permanent.

62.4% of brands now activate 10 or more influencers per campaign (Influencer Marketing Hub)

The days of the single celebrity endorsement are fading. Per Influencer Marketing Hub data, nearly two-thirds of brands running influencer programs now deploy a roster of ten or more creators per campaign, and Sprout Social adds that 52% of B2C companies specifically work with 6 to 10 influencers at a time in any given quarter.

Roster-based campaigns spread risk across creator tiers: one macro-influencer for reach, plus a long tail of micro- and nano-creators for engagement and cost efficiency. 47.4% of brands still spend less than $10,000 per year on influencer marketing, confirming that most programs are small even as the category crosses $30 billion in aggregate.

Sources: Sprout Social, Influencer Marketing Hub.

ROI and Campaign Performance

A decade of benchmark data now shows that influencer marketing outperforms most paid social on earned media value. Measurement remains uneven across the category, but the share of brands that refuse to measure at all is shrinking each year.

Industry aggregators put average earned media value at $6.50 per $1 spent on influencer marketing (Influencer Marketing Hub)

Multiple industry aggregators, citing the Influencer Marketing Hub’s (paywalled) benchmark methodology, put average earned media value at $6.50 per $1 spent on creator partnerships, with top-quartile campaigns reported as high as $18 per $1.

The caveat matters: earned media value is not the same as return on investment. EMV is a gross-attention metric that estimates the cost of equivalent paid reach, not a net financial return after production, fees, and discount codes. Used carefully, it remains the most-cited benchmark for comparing influencer spend against other channels at parity.

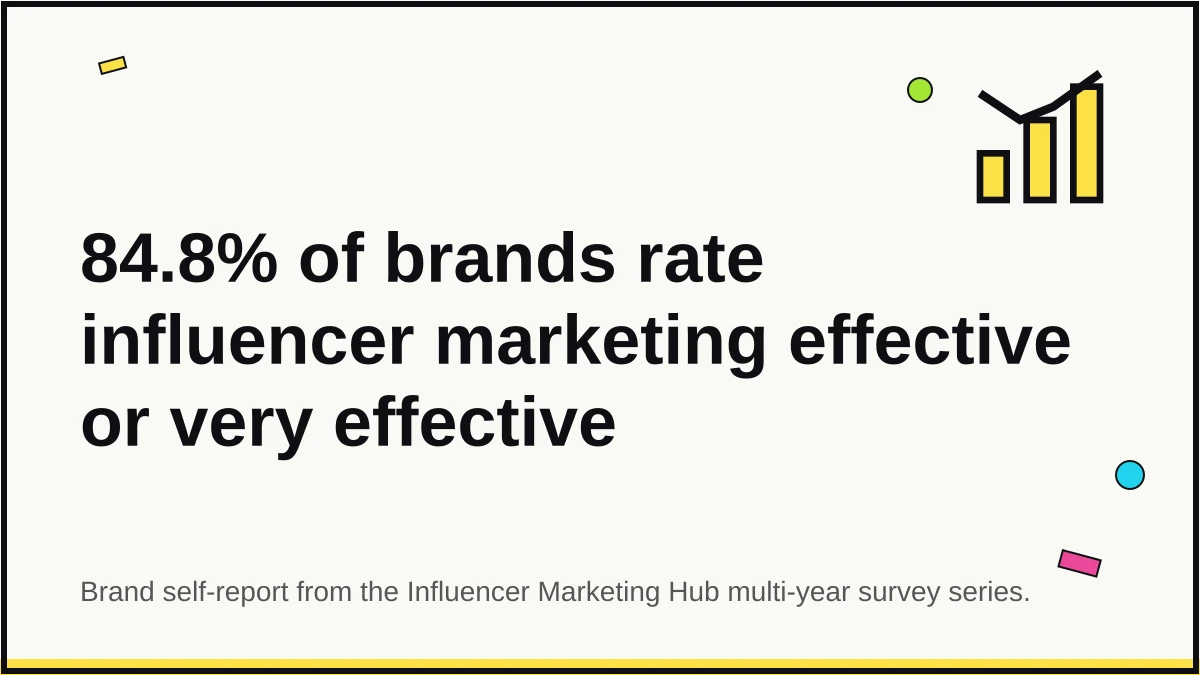

On the sentiment side, the Influencer Marketing Hub’s brand-side surveys find that 84.8% of brands rate the channel as “effective” or “very effective,” and 83.8% say customers acquired through creator campaigns are higher quality than those from other paid channels. The numbers are self-reported, but the direction has held across multiple annual samples.

36% of marketers say influencer content outperforms brand-created content on social (Linqia)

According to secondary reporting of Linqia’s (paywalled) 2023 State of Influencer Marketing Report, more than a third of marketers now say creator content performs better on social than the content their own brands produce. The figure circulates widely across aggregators with consistent attribution, though the underlying PDF sits behind a download wall.

The advantage shows up in two places: live in-feed engagement on creator posts (which frequently double the engagement of comparable brand-handle content), and the durability of creator assets across repurposing cycles (stories, shorts, and B-roll that feed paid campaigns for months after the original post).

Sources: Influencer Marketing Hub, Linqia.

Micro vs Macro Creator Performance

The long-running shift from celebrity endorsements toward micro- and nano-creators accelerated again through 2024 and 2025. Engagement rates explain most of the move: smaller audiences pay more attention.

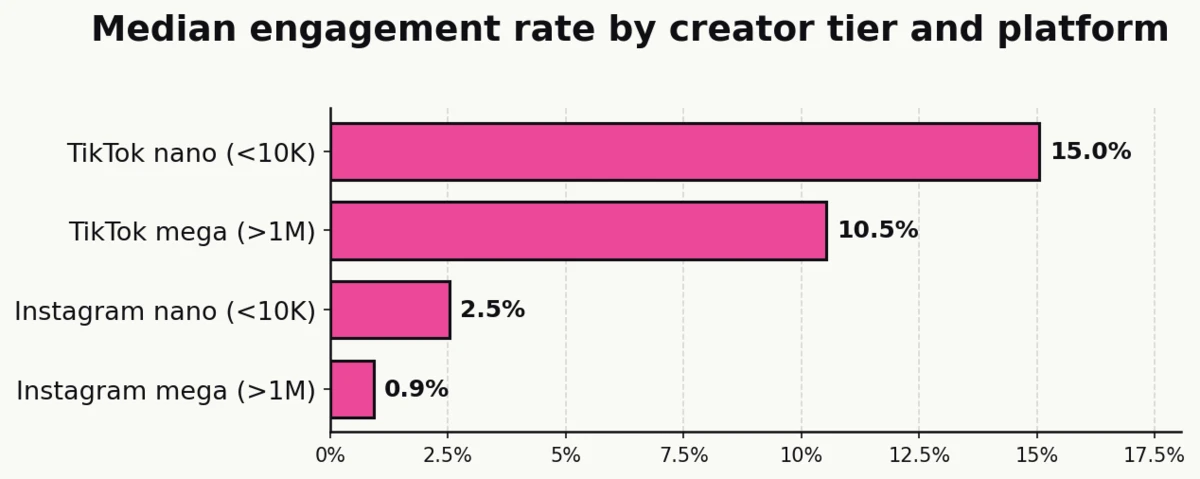

Nano-influencers average 2.53% engagement on Instagram, versus 0.92% for mega-influencers (Influencer Marketing Hub)

The inverse relationship between follower count and engagement has become one of the most durable patterns in the category. Per the Influencer Marketing Hub’s engagement data, Instagram nano-tier creators average 2.53% median engagement, roughly 2.7 times the 0.92% seen on mega-influencers.

TikTok’s engagement numbers run higher across the board: 15.04% for nano-tier creators and 10.53% for mega-tier, reflecting TikTok’s algorithmic feed mechanics and its younger audience.

The practical implication for brand planning is straightforward. A single macro-influencer buys reach. A cohort of twenty nano-creators delivers similar reach at a fraction of the cost while generating multiples of the engagement volume.

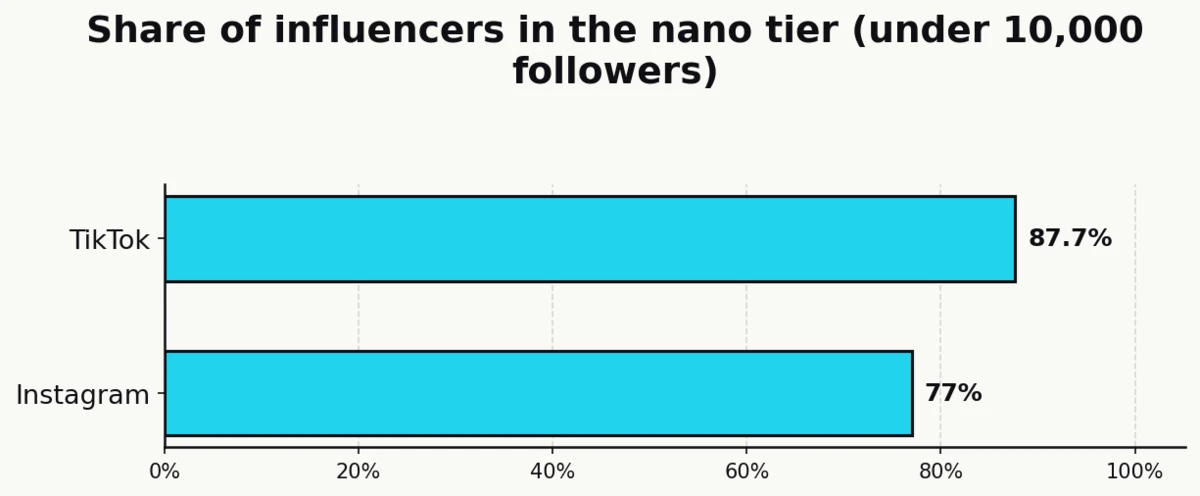

87.68% of TikTok influencers are nano-tier, with fewer than 10,000 followers (Sprout Social)

Per Sprout Social’s 2025 analysis, the share of TikTok’s creator economy that sits in the nano tier is 87.68%. Their average engagement rate is roughly 10.3%, an order of magnitude above what most mid- and macro-creators see on paid-social placements.

Instagram’s supply picture is similar though less extreme: 77% of Instagram influencers are nano-tier. The supply reality makes bulk-activation strategies with tens of nano creators viable on both platforms, and it explains why creator-discovery tooling has become the fastest-growing piece of the influencer martech stack.

53% of influencers prefer short-form video as their top content format for brand partnerships (Sprout Social)

Short-form video has become the de facto standard for creator-brand collaboration. Sprout Social’s creator survey reports 53% of influencers prefer short-form video (15 to 30 seconds) as their top format, and 65% say they want meaningful creative input on brand partnerships. The correlation between creative latitude and campaign performance continues to be a running theme in post-campaign debriefs across agencies and platforms.

Sources: Influencer Marketing Hub, Sprout Social.

Consumer Behavior and Trust

Influencers have become the single most important product-discovery surface for Gen Z and Millennial consumers. Trust patterns have shifted away from celebrity endorsements and toward relatability, expertise, and the appearance of authentic use.

86% of consumers make at least one purchase per year inspired by an influencer (Sprout Social)

Per Sprout Social’s 2025 consumer data, the vast majority of social media users say they have made at least one purchase in the last year directly prompted by a creator post or recommendation. The category’s conversion mechanics work consistently across demographics, and Gen Z consumers are disproportionately likely to act fast. 27% of Gen Z say TikTok is their primary way of engaging with brands, and that cohort acts on creator recommendations faster and more often than the general population.

Pew Research’s Social Media Fact Sheet puts the discovery shift in context: a supermajority of US adults now use at least one social platform, and for younger cohorts the platform itself is the primary news and product-discovery environment. Expectations about disclosure and transparency scale with that reach.

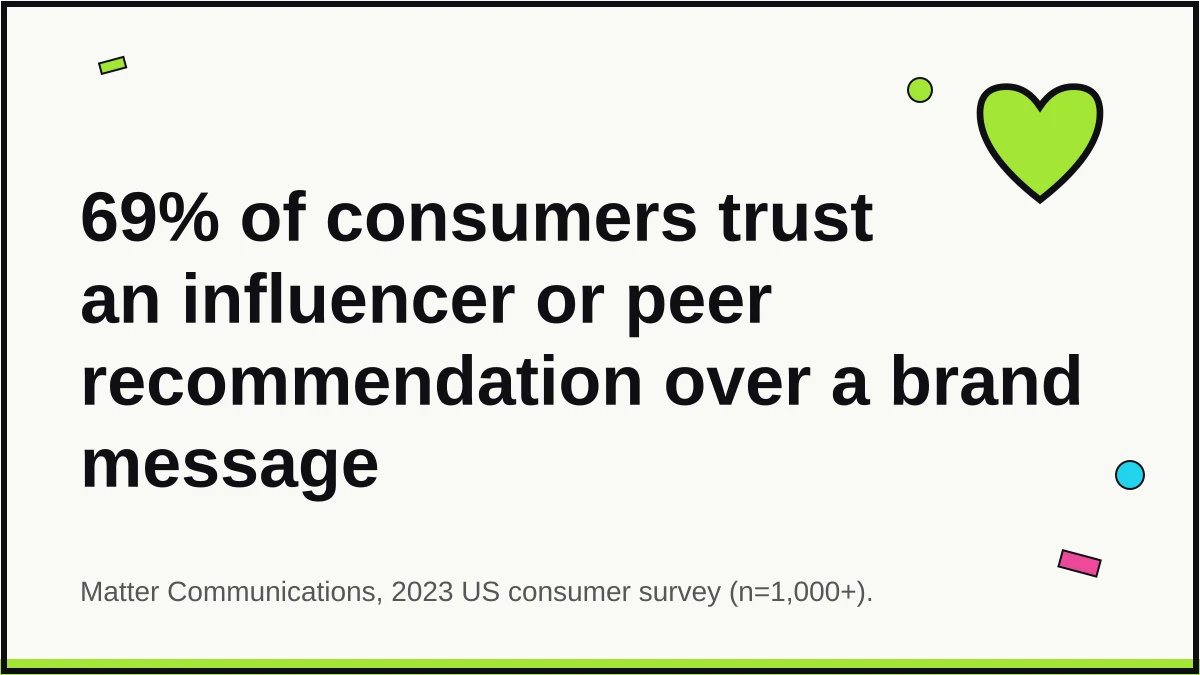

69% of consumers trust a friend, family member, or influencer recommendation over a direct brand message (Matter Communications)

Matter Communications’ “Consumers Continue to Seek Influencers Who Keep It Real” survey, conducted with more than 1,000 US consumers in early 2023, found that 69% of respondents trust an influencer or peer recommendation over information coming directly from a brand. Creator content now sits between peer recommendation and editorial review in the consumer trust hierarchy.

The same survey reported that 81% of respondents have either researched, purchased, or considered purchasing a product after seeing friends, family, or influencers post about it. Creator content is no longer just a top-of-funnel awareness surface; it is a routine input to the purchase decision itself.

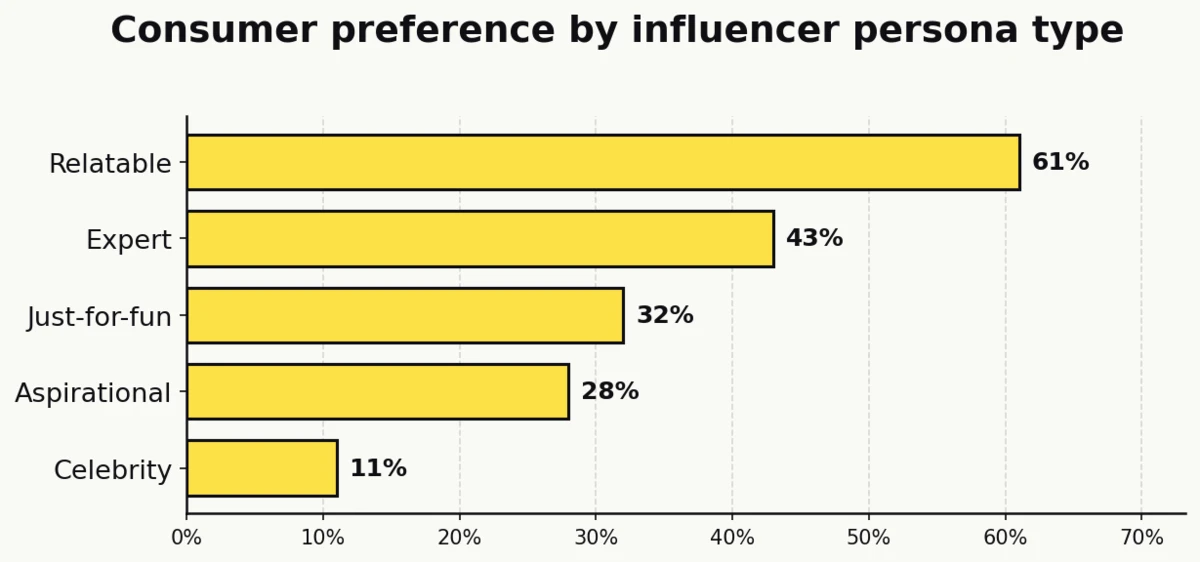

61% of consumers find relatable creators most appealing; only 11% prefer celebrity influencers (Matter Communications)

Matter’s 2023 survey tracked five personality archetypes and a clear winner emerged: relatable (61%), expert (43%), just-for-fun (32%), aspirational (28%), and celebrity at just 11%. The celebrity figure is down from the 17-22% range that chose the same option in Matter’s earlier 2020 study, a clean multi-year trend the trade press has cited repeatedly.

The data underwrites a decade-long shift away from marquee celebrity endorsements and toward creators whose primary credibility is “someone like me who actually uses this.” 67% of consumers also cite honesty and transparency as the single most important quality in a brand-creator partnership, per Sprout Social, which is why disclosure language has moved from a compliance checkbox to a performance variable.

Sources: Sprout Social, Matter Communications, Pew Research Center.

Platform Breakdown

Every major platform now plays a distinct role in the 2026 influencer marketing stack. TikTok owns early discovery and trend cycles, Instagram still delivers the highest-ROI mid-funnel activations, YouTube anchors long-form depth, and LinkedIn has quietly become the sleeper B2B channel.

31% of brands now name TikTok as their preferred influencer platform (Influencer Marketing Hub)

The Influencer Marketing Hub’s 2026 Benchmark Report places TikTok as the top “preferred” platform for influencer campaigns, with Instagram and YouTube in a tightly contested second and third place. The 31% figure represents a shift in how brands pick a primary channel, not a decline from the 68.8% of brands that IMH’s 2024 report said were using TikTok at all. The question wording changed between editions, and the two numbers are not directly comparable.

Platform adoption across the category is effectively saturated. The strategic question brands now face is allocation, not activation.

Instagram’s average influencer engagement rate fell to 2.05% in 2024 (Influencer Marketing Hub)

Per the Influencer Marketing Hub’s year-over-year engagement tracking, Instagram influencer engagement dropped to 2.05% in 2024, continuing a multi-year decline from a post-pandemic peak.

The decline is most pronounced at the top of the creator pyramid, where mega-accounts with more than a million followers now see just 0.92% engagement on Instagram (a number that routinely cleared 2% only a few years ago). Algorithm shifts toward Reels and AI-curated feed selection are the most commonly cited culprits.

Statista’s aggregator page cross-cites the same $1.7B-to-$33B growth series (Statista)

Statista’s global influencer market topic page (which pulls from multiple primary publishers) mirrors the steady $1.7 billion to $33 billion rise that the Influencer Marketing Hub documents in its own series. Journalists covering the category tend to cross-reference both sources; the numbers agree within a rounding error because Statista’s display data sources back to IMH and a handful of platform-level surveys.

Sources: Influencer Marketing Hub (Benchmark), Influencer Marketing Hub (Statistics), Statista.

Fraud, Disclosure, and Regulation

As influencer marketing has scaled, so has the machinery behind fake followers, undisclosed sponsorships, and the regulatory response. Fraud is measurable, shrinking in some places, and quietly growing in others.

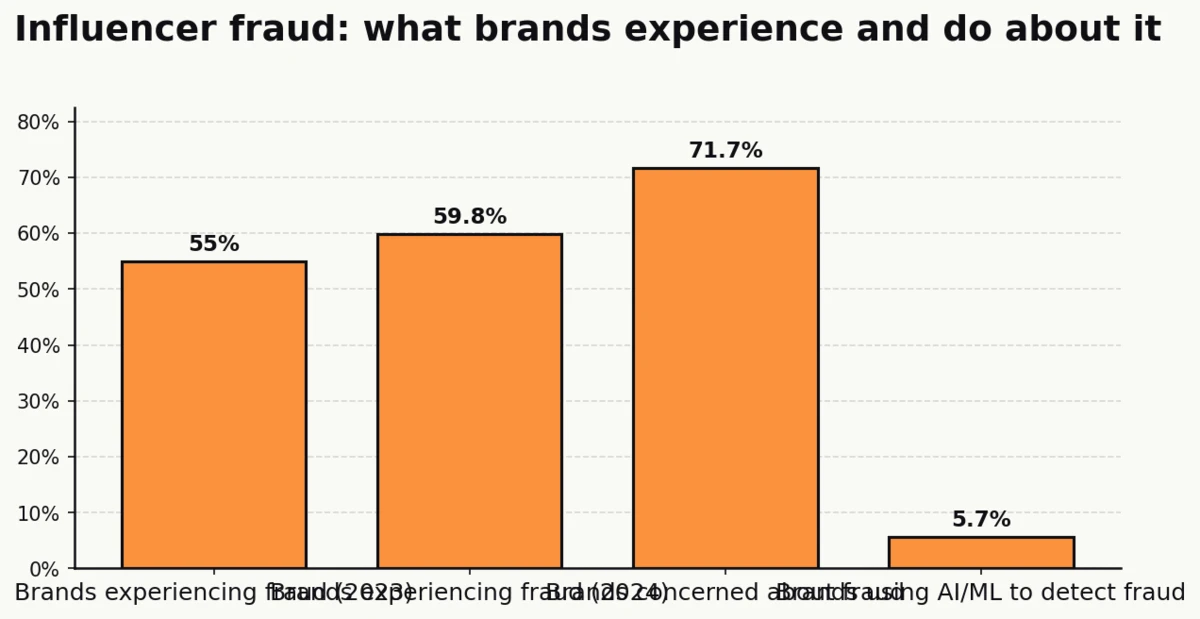

59.8% of brands said they experienced influencer fraud in 2024 (Influencer Marketing Hub)

Per the Influencer Marketing Hub’s brand-side survey, fraud incidence sat at 59.8% in 2024, up from 55% in 2023 (a direction that tracks the category’s growing sophistication and the expanded tooling brands now have to catch fraud they previously missed).

Among brands reporting fraud, 56.5% point to fake followers as the dominant form, per IMH’s 2026 Benchmark Report. Bot engagement and click farms follow. 71.7% of brands remain actively concerned about fraud, even as platform enforcement has improved at the network level.

One definitional caveat matters: “experienced fraud” is brand self-report, not an audited measurement. Brands with better fraud-detection tooling are more likely to catch (and therefore report) fraudulent activity, so the 59.8% figure measures detection capability as much as it measures underlying incidence.

HypeAuditor estimates approximately $1.4 billion is lost to influencer fraud globally each year (HypeAuditor)

HypeAuditor’s State of Influencer Marketing estimate, derived from engagement-rate analysis across 130 million tracked social accounts multiplied by average cost-per-mille, puts global influencer fraud losses at roughly $1.4 billion per year. The figure is an extrapolation (not a direct loss tally) and is reproduced here with that caveat because the underlying research sits behind a download wall.

The extrapolation remains the industry’s reference benchmark in the absence of a fully audited primary measurement, and most trade aggregators cite this number when framing the scale of the fraud problem.

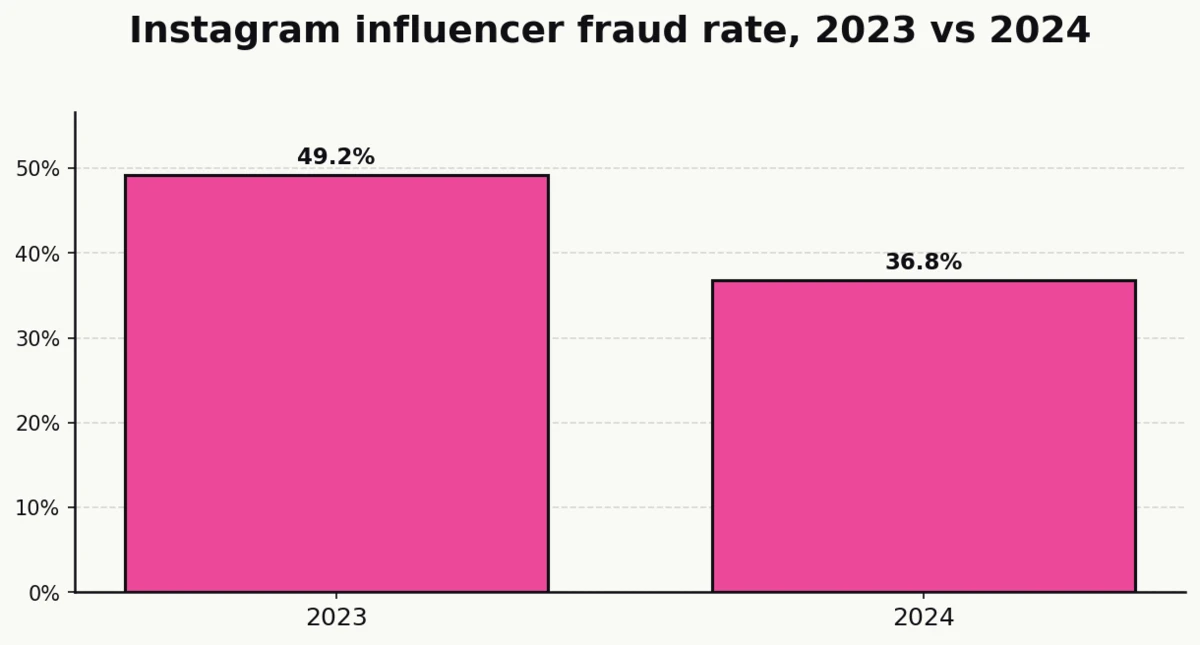

Instagram’s influencer fraud rate dropped from 49.2% in 2023 to 36.8% in 2024 (Influencer Marketing Hub)

Per Influencer Marketing Hub tracking, the share of Instagram influencer accounts classified as fraudulent fell from 49.2% in 2023 to 36.8% in 2024, one of the sharpest platform-level improvements in the category.

Platform enforcement is the main driver. Instagram’s own fake-follower removals, combined with third-party detection tools that now operate upstream of brand activations, have compressed the nominal fraud rate. The tooling gap remains the most counterintuitive finding in the space: only 5.7% of brands use AI or machine learning specifically to detect fraudulent engagement, despite the scale of the problem.

FTC’s 2023 “Disclosures 101” update continues to generate named endorsement actions (Federal Trade Commission)

The Federal Trade Commission’s “Disclosures 101 for Social Media Influencers,” updated in 2023, requires endorsers to disclose material connections to brands “clearly and conspicuously.” Disclosures must appear on the face of the post, not buried in a bio link or hidden behind a swipe-up.

The FTC has opened or settled multiple named endorsement actions against brands, agencies, and individual creators since 2023. Brands running influencer programs at any scale should now treat FTC compliance as a routine marketing-operations responsibility, alongside platform policy review and brand-safety diligence.

Sources: Influencer Marketing Hub, HypeAuditor, Federal Trade Commission.

AI, Virtual Influencers, and Emerging Tech

AI moved from theoretical to operational in influencer marketing between 2023 and 2025. Brands now use it for creator discovery, content co-creation, and fraud detection, and a small but fast-growing slice of activations is running entirely on synthetic creators.

63% of marketers plan to use AI or machine learning in their influencer marketing campaigns in 2025 (Influencer Marketing Hub)

Per Influencer Marketing Hub survey data, nearly two-thirds of marketers plan to use AI or machine learning in at least one influencer campaign, a number that has tripled in two years.

The 2026 Benchmark Report adds that 26.89% of brands now name AI-driven creator matching as their single top focus area for the year, and 36.67% cite AI-enhanced creator discovery as the operational challenge they most want solved.

Virtual influencers report engagement rates roughly 3x those of human influencers of comparable size (HypeAuditor)

According to secondary reporting of HypeAuditor’s (paywalled) multi-year account analysis, virtual influencers on Instagram and TikTok average engagement rates about three times higher than human creators with comparable follower counts. The premium has persisted across several annual samples.

Whether the premium holds as synthetic creators proliferate is an open question. If the category’s novelty erodes, expect engagement compression. If consumer identification with digital personas deepens, the premium sticks and virtual creators become a durable line item on brand media plans rather than an experimental curiosity. The Grand View Research forecast of $45.88 billion in virtual influencer revenue by 2030 assumes the latter.

Sources: Influencer Marketing Hub, HypeAuditor.

Creators at Brand Activations and Live Events

The creator economy has stepped off the screen. Brand activations (pop-ups, launch parties, trade-show booths, experiential campaigns) are now where marketing teams and creators meet in person, and the budget numbers have moved accordingly. This is the category’s most under-documented growth frontier, and also the one most directly tied to how branded content actually gets made in 2026.

Event Marketer’s EventTrack 2026 surveys over 1,000 Fortune 1000 marketers and event attendees (Event Marketer)

EventTrack is the category’s longest-running experiential-marketing benchmark. The 2026 edition, published in October 2025, pulls data from over 1,000 Fortune 1000 marketers and event attendees across B2C, B2B, and trade-show sectors. That is the sample journalists and trade press cite when the conversation turns to in-person brand activation at scale.

The recurring theme across EventTrack’s multi-year reporting is the shift of experiential budgets into line items that produce captured, shareable, measurable content. Creators now sit at the center of that shift.

34% of brands say they are focused on influencer marketing events in 2025 (Event Marketer)

Per the public summary of EventTrack 2025, Event Marketer’s late-2024 research release, 34% of brands say they are focusing on influencer marketing events in 2025, and 33% are running product launch events. The overlap between those two buckets keeps widening as brands invite creators to the same activations they use for product announcements.

The category’s natural home is the intersection of on-site content capture (photo booths, video setups, branded backdrops) and creator attendance. Every piece of user-generated content a creator produces at a brand’s event carries both the creator’s authenticity premium and the branded-set production value, a combination most brands cannot produce at scale through studio shoots alone.

33% of brands ran product launch events alongside influencer activations in 2025 (Event Marketer)

Product launch events with creators on-site form the operational heart of the experiential-creator overlap EventTrack’s research captures. Across over 1,000 Fortune 1000 marketers surveyed, the consistent signal is a move toward activations designed around captured, shareable content. Activations without a built-in photo-and-video capture mechanism are increasingly considered incomplete.

For brands, the operational implication is blunt. Paying for a creator to attend an activation without an integrated mechanism to capture, tag, and syndicate the content they produce is wasted spend. The highest-ROI activations consistently integrate three elements: creator attendance, on-site capture, and same-day distribution across the creator’s channels and the brand’s owned properties.

Sources: Event Marketer (EventTrack 2026), Event Marketer (EventTrack 2025).

Key Takeaways

At $33 billion in projected 2026 value and 86% US marketer adoption, influencer marketing is past the proving-it-works stage. The category is now a permanent line item on the modern marketing P&L, with budgets concentrating rather than diluting as the numbers mature.

Where the money is moving is the more interesting story. Budgets are flowing toward TikTok and micro-creators for engagement, toward AI-assisted discovery tooling for efficiency, and toward creator-attended experiential activations for content production at scale. They are flowing away from single-celebrity endorsements and generalist macro-creators who cannot produce the engagement or the repurposable content that a roster of smaller creators delivers.

Trust and fraud cut both ways. Consumers trust creator recommendations more than direct brand messages at a 69% margin, but fraud incidence sits near 60% and global losses are estimated at $1.4 billion annually. Expect continued investment in AI-driven fraud-detection tooling, and continued friction between platforms, brands, and the FTC over disclosure enforcement.

B2B influencer marketing is the sleeper channel. LinkedIn’s creator and thought-leader formats continue to expand, even as the absolute dollars remain small next to TikTok and Instagram. The B2B marketers adopting influencer-marketing tactics today (thought-leader podcasts, creator newsletters, LinkedIn-native paid programs) are running the same playbook DTC consumer brands ran in 2017-2019.

Live events are where the category is going physical. A third of brands now run dedicated influencer marketing events, on-site content capture has become a mandatory activation element, and creator attendance fees now compete directly with production budgets on the experiential line. For operators working at the intersection of experiential marketing and branded content, 2026 is the year attribution starts to matter at the same level it does for paid social.

The forward look is simple: if the $33 billion 2026 projection is on the low side of what the category delivers, the upside will come from two places that the 2024 benchmark reports barely measured. First, AI-native creator operations (discovery, matching, post-production). Second, the physical-world creator economy (activations, pop-ups, and creator-attended brand experiences). Watch both.

Sources

- Event Marketer (2024). “EventTrack 2025: Exclusive Research.” https://www.eventmarketer.com/article/eventtrack25/

- Event Marketer (2025). “EventTrack 2026: Exclusive Research.” https://www.eventmarketer.com/article/exclusive-research-eventtrack-2026/

- Federal Trade Commission (2023). “Disclosures 101 for Social Media Influencers.” https://www.ftc.gov/business-guidance/resources/disclosures-101-social-media-influencers

- Goldman Sachs (2023). “The creator economy could approach half-a-trillion dollars by 2027.” https://www.goldmansachs.com/intelligence/pages/the-creator-economy-could-approach-half-a-trillion-dollars-by-2027.html

- Grand View Research (2025). “Virtual Influencer Market Size, Share & Trends Analysis Report, 2025–2030.” https://www.grandviewresearch.com/industry-analysis/virtual-influencer-market-report

- HypeAuditor (2024). “State of Influencer Marketing.” https://hypeauditor.com/resources/

- Influencer Marketing Hub (2026). “The State of Influencer Marketing Benchmark Report 2026.” https://influencermarketinghub.com/influencer-marketing-benchmark-report/

- Influencer Marketing Hub (2024). “Influencer Marketing Statistics.” https://influencermarketinghub.com/influencer-marketing-statistics/

- Linqia (2023). “2023 State of Influencer Marketing Report.” https://www.linqia.com/

- Matter Communications (2023). “Consumers Continue to Seek Influencers Who Keep It Real.” https://www.matternow.com/blog/consumers-seek-influencers-who-keep-it-real/

- Pew Research Center (2024). “Social Media Fact Sheet.” https://www.pewresearch.org/internet/fact-sheet/social-media/

- Sprout Social (2025). “Influencer Marketing Statistics.” https://sproutsocial.com/insights/influencer-marketing-statistics/

- Statista (2025). “Influencer marketing market size worldwide.” https://www.statista.com/statistics/1092819/global-influencer-market-size/